Weekly Newsletter – September 11, 2017

Weekly Review

Over the last week, there was a larger focus among investors on macro events than on individualized economic reporting.

The sentiment of the stock market was impacted in a negative way by continued political trouble with North Korea, primarily with its nuclear weapons testing program, and the recent impact of catastrophic Hurricane Irma.

A lessened confidence in Congress to enact meaningful tax reform has also added to the impact of recent politics on the stock market.

Long-term Treasury yields have been pushed lower following a speech by Neel Kashkari. In his speech, Kashkari, Minneapolis Fed President and FOMC member, stated that his belief that recent Fed rate hikes have been detrimental to the U.S. economy.

These lowered long-term Treasury yields, paired with decreased expectations for further increases in the short-term rate come December, have led to a decline in the U.S. dollar over the last week.

This most recent decline in the U.S. dollar has brought it to its lowest level in comparison with a number of foreign currencies since 2015. The U.S. dollar has already fallen roughly 10% against the euro in less than eight months.

The Fed Funds futures market currently shows a probability of another rate hike this year at just 27.3%, down from 40.8% last week. The current implied probability for a rate-hike at the June 2018 FOMC meeting fell to 47.1% from last week’s 58.3%.

In housing, CoreLogic reported their Home Price Index (HPI) showed home prices increased significantly both month-over-month and year-over-year in July.

Nationally, the average cost of a single-family house increased nearly 0.9% from this time last month and 6.7% from this time last year. The CoreLogic HPI Forecast suggests the trend of higher home prices will continue, leading to another 5% national gain in home prices year-over-year by July 2018.

CoreLogic CEO Frank Martell stated “Home prices in July continued to rise at a solid pace with no signs of slowing down. The combination of steadily rising purchase demand along with very tight inventory of unsold homes should keep upward pressure on home prices for the remainder of this year.

While mortgage interest rates remain low, affordability cracks are emerging as over a third of U.S. top cities are now overvalued.”

As for mortgages, mortgage application volume increased during the week ending September 1. The Mortgage Bankers Association (MBA) reported their overall seasonally adjusted Market Composite Index (application volume) rose 3.3%.

The seasonally adjusted Purchase Index increased 1.0% from the prior week while the Refinance Index advanced 5.0%.

Overall, the refinance portion of mortgage activity increased to 50.9% of total applications from 49.4% in the prior week. The adjustable-rate mortgage share of activity increased to 7.2% of total applications from 6.9%.

According to the MBA, the average contract interest rate for 30-year fixed-rate mortgages with a conforming loan balance fell to 4.06% from 4.11% with points decreasing to 0.38 from 0.43.

For the week, the FNMA 3.5% coupon bond gained 35.9 basis points to close at $103.828. The 10-year Treasury yield decreased 11.16 basis points to end at 2.0541%. The major stock indexes ended the week lower.

The Dow Jones Industrial Average lost 189.77 points to close at 21,797.79. The NASDAQ Composite Index dropped 75.14 points to close at 6,360.19 and the S&P 500 Index fell 15.12 points to close at 2,461.43.

Year to date on a total return basis, the Dow Jones Industrial Average has gained 10.3%, the NASDAQ Composite Index has advanced 18.15%, and the S&P 500 Index has added 9.94%.

This past week, the national average 30-year mortgage rate decreased to 3.84% from 3.90%; the 15-year mortgage rate decreased to 3.12% from 3.18%; the 5/1 ARM mortgage rate moved lower to 3.10% from 3.18% and the FHA 30-year rate fell to 3.35% from 3.50%. Jumbo 30-year rates decreased to 4.10% from 4.18%.

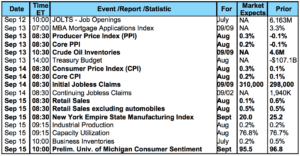

Economic Calendar – for the Week of September 11, 2017

Economic reports having the greatest potential impact on the financial markets are highlighted in bold.

Mortgage Rate Forecast with Chart – FNMA 30-Year 3.5% Coupon Bond

The FNMA 30-year 3.5% coupon bond ($103.828, +35.6 bp) traded within a 37.5 basis point range between a weekly intraday low of $103.578 on Tuesday and a weekly intraday high of $103.953 on Thursday and Friday before closing the week at $103.828 on Friday.

The bond managed to move higher this past week despite very choppy trading and while continuing to be extremely “overbought.” The holiday-shortened week’s trading action was highlighted by alternating days of the bond moving higher, then lower.

This choppy trading also resulted in alternating daily buy and sell signals from positive and negative crossovers in the slow stochastic oscillator.

It is difficult if not impossible to forecast directional movement in such a choppy trading environment. Given that September is historically the worse performing month for the stock market; we could see mortgage bond and Treasury prices continue to improve slightly resulting in stable to slightly lower rates.

However, from a purely technical perspective, mortgage bonds are not likely to remain at such extremely overbought levels for much longer and will be susceptible to a move lower toward support levels resulting in rates edging a little higher from current levels.

The post Weekly Newsletter – September 11, 2017 appeared first on Owings Mills & Lutherville Mortgage.

Are You Ready to Get the Ball Rolling on Your Mortgage?

Get in Touch With a Mortgage Expert

NMLS# 150953

© 2024 All Rights Reserved | Luminate Home Loans, Inc.